Keywords: Global Economic Crisis

There are more than 200 results, only the first 200 are displayed here.

-

ECONOMICS

- David James

- 29 April 2020

6 Comments

The COVID-19 pandemic is starting to ease, but the economic and financial fall out has just begun. It is not as if the world economy was in good shape before economic activity was slashed and entire industries were shut down. Those fault lines are only going to worsen, and the consequences might be very dark.

READ MORE

-

ECONOMICS

- David James

- 01 April 2020

4 Comments

The world-wide chaos caused by the outbreak of the coronavirus has underlined a lesson that was only partly learned in the Global Financial Crisis of 2008. In a more interconnected world the understanding of system-wide risk needs to be much better than it is.

READ MORE

-

AUSTRALIA

- Andrew Hamilton

- 25 March 2020

33 Comments

To think of life after COVID-19 is daunting. The changes that it has brought to our daily lives have been vertiginous. Our awareness of its potential harm is still limited. We are only beginning to catch sight of the grim beast that slouches towards us threatening death and devastation in coming months.

READ MORE

-

ARTS AND CULTURE

- Deborah Singerman

- 15 March 2020

2 Comments

I still mainly look back. The bushfire legacy lives on. It acts as a benchmark for assessing tragedy and hope. I cannot get the searing images out of my head of red, angry skies, of flames raging frighteningly, embers flying, and firefighters miraculously persevering against the odds.

READ MORE

-

AUSTRALIA

- Cristy Clark

- 12 March 2020

24 Comments

This behaviour did not come out of nowhere. It has been carefully cultivated through over 40 years of neoliberal economic policies that have made it blatantly clear to people that they are on their own and will absolutely be left to fall if they don’t scramble their way to the top of the heap — supported, if necessary, by their own accumulated rolls of toilet paper.

READ MORE

-

ECONOMICS

- David James

- 03 March 2020

10 Comments

We live in an era of hyper-transactionalism, whereby most of what we do is subject to the exchange of money and market pricing. Whereas in the past much of humanity was bound to a political system, now most of us are bound to a globalised monetary system.

READ MORE

-

FAITH DOING JUSTICE

- Andrew Hamilton

- 19 February 2020

5 Comments

Catholic reflection on social justice has been supercharged by Pope Francis, who in his encyclical Laudato Si declared the Cry of the Poor and the Cry of the Earth to be central to faith. He also insisted that neither could be addressed simply by technological fixes but required personal conversion to see the world as gift to be respected, a home, and not as a prison or a mine.

READ MORE

-

ECONOMICS

- David James

- 04 February 2020

3 Comments

A shift is afoot in the west's financial markets that represents the most important economic change since the emergence of the new financial instruments in the 1990s that ultimately led to the global financial crisis. It is likely to result in a new way of thinking about money, which will change the substructure of developed economies.

READ MORE

-

ENVIRONMENT

- Cristy Clark

- 13 January 2020

7 Comments

There are so many details about these unprecedented bushfires that I have no idea how to process. But nothing — including the ever-present shroud of acrid smoke that has blanketed my city since November — has brought home the scale of this tragedy quite like the estimation that one billion native animals have been killed.

READ MORE

-

ENVIRONMENT

- Tim Hutton

- 07 January 2020

43 Comments

Here is why the Morrison government was so slow off the mark: to acknowledge the unprecedented nature of these fires is to concede that there is something happening to the climate. The only way to downplay the reality of climate change, was to downplay the severity of the fires themselves.

READ MORE

-

ECONOMICS

- David James

- 21 October 2019

5 Comments

Recognising that financial systems are a human creation rather than natural systems governed by 'capital flows' would be an important step to conceiving a more robust and equitable system. To ask what kind of society we want and only then work out what we want money to do for us is to put the horse back in front of the cart.

READ MORE

-

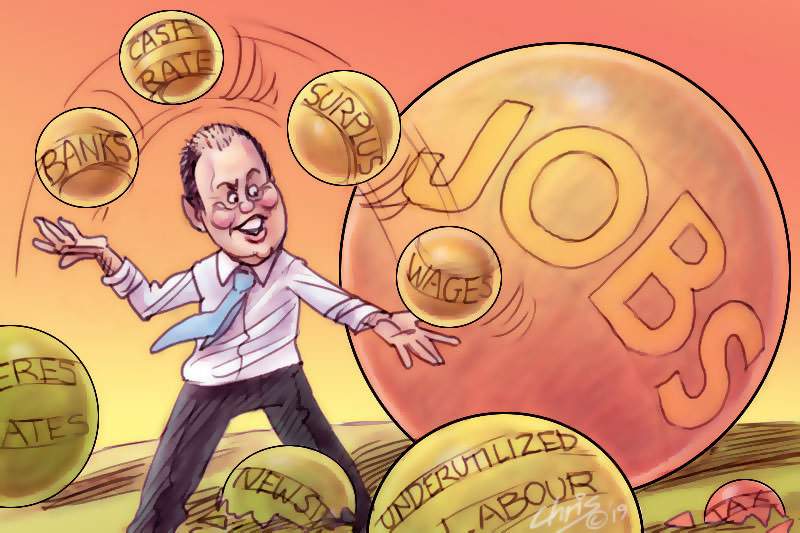

AUSTRALIA

- Joe Zabar

- 18 October 2019

3 Comments

Treasurer Josh Frydenberg's attack on banks for failing to pass on the full rate cut to consumers is a political distraction. There are two clear signals coming out of the latest cut. First, monetary policy is not enough to spark a revival of the economy. Second, it's now all about jobs. Frydenberg and his officials would be wise to heed these signals.

READ MORE